Res Dev Med Educ. 13:29.

doi: 10.34172/rdme.33240

Original Article

A comprehensive performance audit model in the public health sector using the grounded theory approach

Hojjat Esmati Beyrami Conceptualization, Data curation, Investigation, Writing – original draft, Writing – review & editing,

Aliasghar Motaghi Conceptualization, Methodology, Project administration, Supervision, *

Younes Badavar Nahandi Resources,

Ahmad Mohamadi Software,

Author information:

Department of Accounting, Faculty of Management, Economics and Accounting, Tabriz Branch, Islamic Azad University, Tabriz, Iran

Abstract

Background:

Performance auditing is one requirement for public sector managers to be accountable to the public. It offers an unbiased evaluation of the responsibilities, effectiveness, or expenses linked to implementing policies, programs, or operations in the public sector. This paper aims to develop a performance auditing model in the health sector.

Methods:

This qualitative study is based on grounded theory. A sample of 16 individuals, including university professors specializing in performance auditing and managers and experts, particularly those with a background in the public health sector service designing and development, were selected using theoretical sampling. The interviews were analyzed using Strauss and Corbin’s three-stage coding process, and summarization and analysis were carried out using MAXQDA software.

Results:

Based on the results, the concepts related to contextual conditions include formulating appropriate laws and regulations (as the main category) and two subcategories. In causal conditions, empowerment and utilizing specialized and efficient human resources (as the main category) and five subcategories were extracted. The central phenomena consist of laying the groundwork for performance auditing (main category) and three subcategories. Two main categories for strategies and actions were identified: managing internal organizational goals and controlling internal policies, with two subcategories for each. In the intervening conditions, intra-organizational economic factors (main category) and three subcategories were determined. Finally, the outcomes include organizational structuring and productivity (two main categories), with two subcategories for each.

Conclusion:

several factors are crucial for improving performance auditing in the health sector, including empowering and utilizing specialized and efficient human resources, implementing appropriate laws and regulations, managing organizational goals, structuring the organization effectively, controlling internal policies, considering internal economic factors, establishing a framework for performance auditing, and enhancing organizational productivity.

Keywords: Performance auditing, Public health sector, Grounded theory approach

Copyright and License Information

© 2024 The Author(s).

This is an open access article distributed under the terms of the Creative Commons Attribution License (

http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, as long as the

original authors and source are cited. No permission is required from the authors or the publishers.

Funding Statement

There was no funding source.

Introduction

It is a fundamental principle of democracy that governments must be held accountable to the individuals who have granted them authority. Citizens have the right to use their civic rights and demand accountability regarding public financial resources, the efficiency and effectiveness of elected officials, and the extent to which programs are implemented to enhance their well-being1 Accountability and responsibility are closely related concepts. According to the Oxford Dictionary, accountability means “the obligation of a person to provide an account or explanation for their actions regarding a responsibility they have accepted.” In contrast, responsibility is a moral or legal commitment to care for something or fulfill a duty for which an individual may be blamed in case of harm or negligence.2 Accountability encompasses two duties: one is to perform a specific action, and the other is to provide logical reasons for the action. Performance accountability, which falls under managerial accountability, emphasizes the efficient and effective use of financial resources. In other words, efficiency and effectiveness are central to financial resources, and executives in governments and large public sector institutions must adhere to laws and regulations while utilizing public financial resources efficiently, effectively, and economically and be accountable for achieving these goals.3 Initially, high-level auditing institutions focused more on assessing governments’ legality of resource use. However, over time, the importance of efficiency and effectiveness in government resource utilization became apparent, leading to the development of performance auditing.4

Performance auditing involves formulating and developing models to evaluate economic efficiency and effectiveness in business operations. Thus, performance auditing is crucial in assessing responsibility in a democratic society, which is necessary for accountability. This auditing approach provides objective analysis so that managers and oversight officials can use relevant information to improve program and operational performance, reduce costs, make decisions on supervision or initiate corrective actions, and facilitate public accountability.5 Officials and legislators require information that confirms the proper and lawful use of public funds. They want to know if government organizations have achieved the intended goals of their plans and services and whether these organizations manage their plans and services economically. On the other hand, citizens demand greater government accountability for programs funded by their tax money.6 The primary objective of performance auditing is to effectively evaluate operational methods and improve them, with their success measured by implementing the proposed recommendations. In other words, performance auditing enhances future performance and concerns policies, planning, control systems, and decision-making methods. A review of existing laws regarding the duties and objectives of national oversight organizations, particularly the Supreme Audit Court and the Audit Organization, indicates the lack of necessary laws or the ineffectiveness of existing laws.7 Performance auditing in government agencies is essential because it can enhance the integrity and trustworthiness of these organizations. In other words, performance auditing helps the government gain public trust, strengthen the relationship between the government and citizens, and determine its efficiency and effectiveness in achieving its goals.8

The share of healthcare costs as a percentage of gross domestic product (GDP) is often higher in developed countries than in developing countries. This indicates that the importance of human health in a society increases with a country’s development. Most high-income countries that are members of the Organization for Economic Co-operation and Development (OECD) spend more than 7% of their GDP on healthcare.9 In Iran, the health sector significantly advances national macro policies with a 10% share of the national budget (or 6% of the country’s GDP). The Iranian healthcare system operates in an environment with rapid social, economic, and technical changes, which creates multiple challenges and tensions. Fundamental, targeted, and sustainable reforms in the healthcare system are necessary to address issues related to justice, quality, appropriateness, and effectiveness.10 The ranking of Iran at 93 in terms of overall health and 58 in providing healthcare services among global health systems indicates significant weaknesses and inefficiencies in achieving the fundamental goals of the health system.11 Therefore, the role and importance of performance auditing in the health sector, especially under the current conditions in the country, is crucial. Individuals in this field bear significant responsibilities regarding accountability, sensitivity, precision, and integrity. Proper management of resources to ensure that healthcare services are not compromised is of utmost importance due to the diversity of services and substantial cash flows. The primary goal in this area is to ensure the population’s health, and auditing plays a unique role in achieving this goal. Performance auditing helps preserve financial resources and directs the healthcare sector toward success by adopting appropriate financial strategies. Considering the issues above, inherent weaknesses in financial auditing, and existing limitations, as well as the requirement for governments to adhere to laws and regulations regarding the acquisition and use of financial resources and the lack of focus on efficiency, effectiveness, and economy in financial statement auditing, this research aims to provide a comprehensive model for performance auditing in the public health sector.

Methods

The qualitative study employed the grounded theory approach. The study population comprises university professors specializing in auditing, with expertise in conducting research in the public health sector and supervising theses on performance audits in this domain. Additionally, the population comprises managers and experts with experience in performance auditing, particularly those with a background in the public health sector and the design and development of services.

The method is theoretical sampling, The sampling process continues until theoretical saturation is achieved.12 Theoretical saturation in grounded theory refers to a state where the researcher subjectively determines that new data does not provide additional information or insights for developing categories.13 Data collection involves interviews. Given the topic and objectives of the research, a semi-structured interview method is used. It is worth noting that due to the request of the interviewees to keep their identities confidential, names were not disclosed in this study; instead, understandable codes were used for the researcher and the reader. Interviews were conducted in person, with some recorded (with the interviewees’ consent) and others noted down. The interviews with experts and specialists were transcribed, and the collected data were analyzed and synthesized. The interview process was designed so that after each interview, the data would be coded and analyzed to identify the dimensions discussed by the initial experts. These dimensions were then followed up in subsequent interviews.14 Considering the above, 16 people were invited to participate in interviews as planned.

The sample size and demographic characteristics are detailed in the Table 1.

Table 1.

Demographic characteristics of the sample

|

Demographic characteristics |

Interview

|

|

Frequency

|

Percent

|

| Gender |

Male |

14 |

88 |

| Female |

2 |

13 |

| Age |

Under 35 years |

0 |

0 |

| 35 to 45 years |

5 |

31 |

| 45 years and older |

11 |

69 |

| Work experience |

Less than ten years |

0 |

0 |

| 10 to 15 years |

2 |

13 |

| 15 to 20 years |

5 |

31 |

| 20 to 25 years |

6 |

38 |

| More than 25 years |

3 |

19 |

| Education level |

Bachelor's |

0 |

0 |

| Master's |

9 |

56 |

| Doctorate |

7 |

44 |

| Total |

|

16 |

100 |

Open coding

This stage involves categorizing codes into potential themes and organizing all summarized coded data into specified themes. In this phase, the researcher begins analyzing their codes and considers how different codes can be combined to create overarching themes. This process includes screening, removing redundant codes, and integrating synonymous codes, leading to the categorization of indicators extracted from interview texts. Subsequently, using the grounded theory approach, tables of categories derived from interviewees will present a model for a comprehensive performance auditing framework in the public health sector.

Axial coding

Axial coding is the second stage of analysis in grounded theory. This stage aims to establish relationships between the categories generated in the open coding stage. In this stage, the indicators extracted from the interview texts are categorized through screening, removing duplicate codes, and integrating similar codes. The relationship of other categories with the core category can be realized under six headings: causal conditions, the core phenomenon, strategies, actions, intervening conditions, contextual conditions, and consequences.15

Results

After obtaining all the indicators from the open coding stage, the next step was determining the categories as shown in Table 2.

Table 2.

Initial (open) and axial coding of research interview texts

|

Axial coding

|

Open coding

|

| Increasing knowledge and skills |

-

Creating sufficient knowledge and skills for auditors

-

Enhancing the knowledge, skills, and performance of managers and executives

|

| Performance auditing training |

-

Training on performance auditing standards

-

Creating and developing courses and fields related to performance auditing

-

Requiring auditors of the Court of Audit to attend specialized courses

-

Creating professional certifications related to performance auditing

|

| Utilizing specialized workforce |

|

| Financial reporting transparency |

|

| Quality management to achieve objectives |

-

Planning for nurturing creativity and talents within the organization's human resources

-

Planning for attracting financial resources needed for projects and capital plans

-

Developing programs to remove obstacles to budget implementation

-

Planning and managing results and objectives

|

| Preparing and strengthening the budget control system |

-

Preparing a comprehensive performance-based budgeting system plan

-

Strengthening the accountability system within the budget framework

-

Institutionalizing cost accounting in the budgeting process

|

| Creating an environment for performance auditing |

-

Mandating performance auditing alongside compliance and financial auditing

-

Establishing the necessary legal capacities for performance auditing

-

Institutionalizing performance auditing

|

| Support and acceptance for conducting performance auditing |

|

| Utilizing an accurate information system |

-

Lack of access to informational resources

-

Ensuring the complete entry of data into the system and processing and producing reliable and timely information.

-

Assisting managers' strategic programs through the information system

|

| Determining and comparing predefined goals |

-

Determining the extent of goal achievement

-

Comparing performance with predefined goals

-

Developing the organization's mission, strategies, and goals clearly

|

| Increasing guarantees and strengthening performance auditing |

-

Enhancing professional judgment and analytical abilities of auditors

-

Increasing the necessary guarantees for performance auditing

-

Engaging executive officials in the performance auditing process

-

Increasing the necessary guarantees for evaluating performance auditing

|

| Increasing motivation for research and investigation |

-

Enhancing the role of research and studies in the development, efficiency, and use of technology

-

Creating a social environment for nurturing talents

-

Encouraging and motivating research and investigation

|

| Implementing and establishing a cost accounting system for goods and services |

-

Implementing a cost accounting system for goods and services

-

Full implementation of accrual accounting

-

Establishing an appropriate cost accounting system in organizations

|

| The role and position of resource measurement and valuation |

-

Designing an operational structure for performance measurement and analysis

-

Using an economic resource measurement approach in accounting

-

Identifying, measuring, and valuing capital assets

|

| Defining and improving key organizational performance indicators |

-

Setting performance efficiency standards

-

Identifying key performance indicators

-

Setting sustainability indicators (social, economic)

|

Contextual conditions categories

Based on the results of the secondary coding of the research as shown in Table 3, the indicators of establishing standards, laws, and regulations, as well as exercising control and supervision over policies and rules, were chosen as the contextual categories in providing a comprehensive performance audit model in the public health sector.

Table 3.

Categories of contextual conditions

|

Paradigm

|

Main Category

|

Subcategory

|

| Contextual conditions |

Developing appropriate laws and regulations |

-

Establishing standards, laws, and requirements

-

Exercising control and supervision over policies and laws

|

Categories of causal conditions

Based on the results of the secondary coding in the research as shown in Table 4, the indicators of increasing knowledge and skills, training in performance auditing, efficient human resources, utilizing a specialized workforce, and expanding specialized teams through collaboration and relationship-building were identified as categories of causal conditions. These elements were selected as crucial for developing a comprehensive performance audit model in the public health sector.

Table 4.

Categories of Causal Conditions

|

Paradigm |

Main Category

|

Subcategory

|

| Causal conditions |

Empowerment for employing skilled and efficient human resources |

-

Utilization of specialized personnel

-

Increasing specialized teams through cooperation and establishing relationships

-

Enhancing knowledge and skills

-

Performance audit training

-

Efficient human resources

|

Central phenomenon categories

Based on the results of the secondary coding in the research as shown in Table 5, the indicators of creating an environment for conducting performance audits, support and acceptance for conducting performance audits, and increasing guarantees and strengthening performance auditing were identified as the central phenomenon categories. These categories were selected as crucial components in providing a comprehensive performance audit model in the public health sector.

Table 5.

Categories of central phenomenon

|

Paradigm

|

Main Category

|

Subcategory

|

| Central phenomenon |

Creating a basis for performance audit implementation |

-

Creating an environment for implementing performance audit

-

Support and acceptance for conducting performance audit

-

Increasing enforcement and strengthening performance audit

|

Strategies and actions categories

Based on the results of the secondary coding of the research as shown in Table 6, the indicators of the system for budget control preparation and strengthening, financial reporting transparency, quality management for achieving objectives, and the determination and comparison of predetermined objectives were selected as categories of strategies and actions in presenting a comprehensive performance audit model in the public health sector.

Table 6.

Categories of strategies and actions

|

Paradigm

|

Main category

|

Subcategory

|

| Strategies and actions |

|

-

Quality management for achieving goals

-

Setting and comparing predetermined goals

-

System for developing and strengthening budget control

-

Transparency in financial reporting

|

Categories of intervening conditions

Based on the results of the secondary coding in the research as shown in Table 7, the indicators for the appropriate utilization of operational budgeting, the determination of economically feasible measures, and the role and position of measuring and valuing resources were selected as categories of intervening conditions in presenting a comprehensive performance auditing model in the public health sector.

Table 7.

Categories of intervening conditions

|

Paradigm

|

Main Category

|

Subcategory

|

| Intervening conditions |

Intra-organizational economic factors |

-

Appropriate utilization and application of operational budgeting

-

Determination of economically feasible measures

-

Role and position of measuring and valuing resources

|

Categories of consequences

Based on the results of the secondary coding in the research as shown in Table 8, the indicators for the implementation and establishment of cost accounting for goods and services, the determination and improvement of key organizational performance indicators, the enhancement of research and investigation motivation, and the use of an accurate information system were selected as categories of consequences in presenting a comprehensive performance auditing model in the public health sector.

Table 8.

Categories of Consequences

|

Paradigm

|

Main category

|

Subcategory

|

| Consequences |

|

-

Increasing motivation for research and investigation

-

Utilization of an accurate information system

-

Implementation and establishment of cost accounting for goods and services

-

Determination and improvement of key organizational performance indicators

|

Selective coding

Integrating data is crucial in grounded theory. After data collection, the process involves analysis, interpretation, model presentation, conclusions, and summarization. The current situation is initially examined, and the collected data is categorized into six main categories. With input from experts and specialists, all the indicators derived from the qualitative data analysis of interviews are consolidated. This includes eight main components, 21 primary indicators, and 65 sub-indicators, which are used to present a comprehensive performance auditing model in the public health sector.

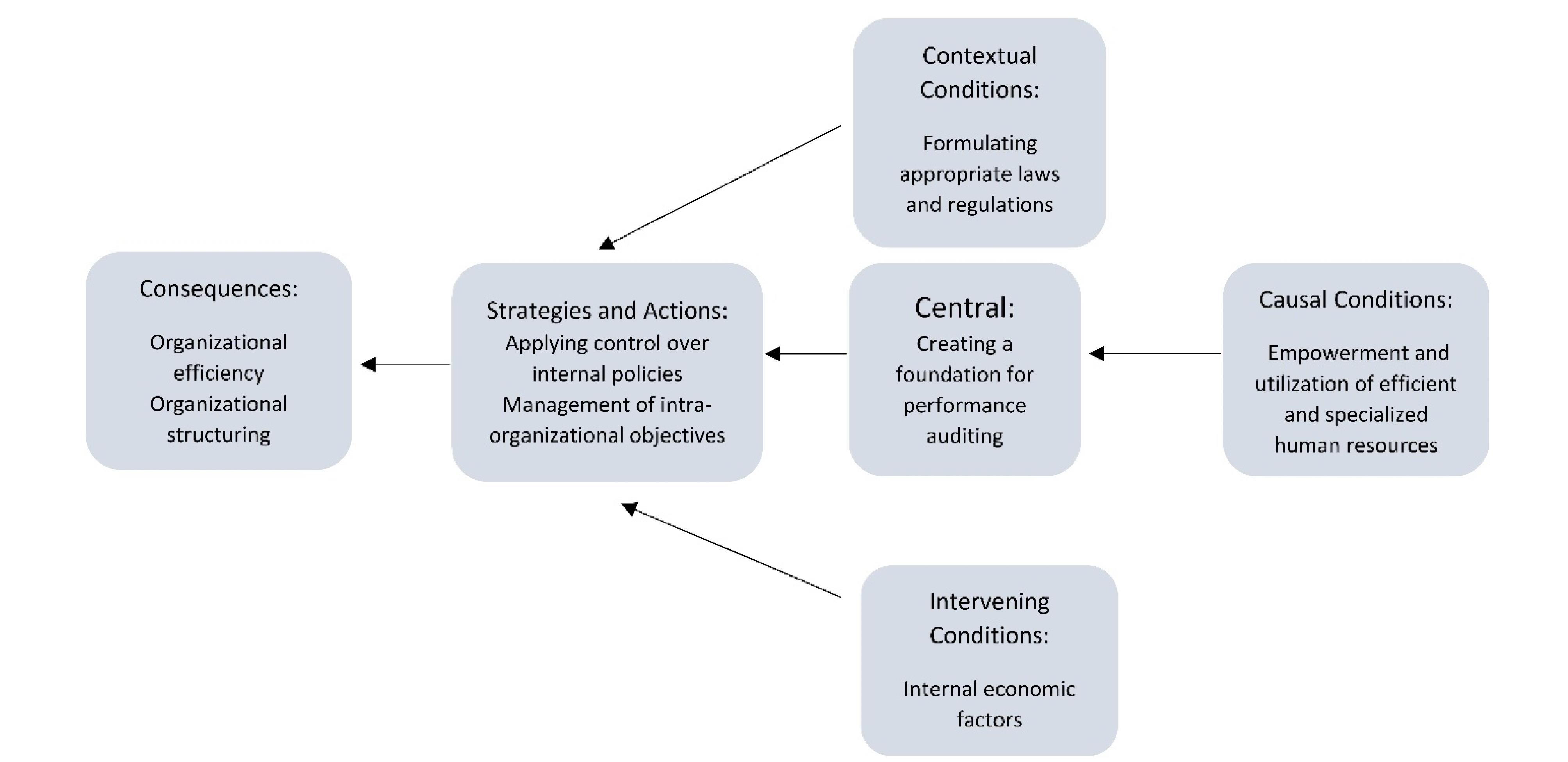

Figure 1 represents the comprehensive paradigmatic model of performance auditing in the public health sector.

Figure 1.

Comprehensive paradigmatic model of performance auditing in the public health sector

.

Comprehensive paradigmatic model of performance auditing in the public health sector

Discussion

In our country, the management of a significant portion of economic resources is the responsibility of the government, and the quality of this management has a fundamental impact on the fate of the people. Public sector managers must be accountable to the people and their representatives, providing the tools for this accountability based on reliable information. Public expectations for better quality services emphasize the continuous improvement of public services and an increasing emphasis on responsibility for the consequences of public sector organizations. This includes adopting better methods in auditing and providing comprehensive and improved feedback on their operations’ performance.

Performance auditing is a mechanism implemented to ensure the accountability of executive bodies to the legislature. Government agencies receive resources to perform specific duties and provide various reports, including financial statements and statistics on the results of their actions and the achievement of set goals, to different oversight bodies. The nature of the public sector necessitates performance auditing, in addition to examining financial statements and expressing opinions within the framework of auditing principles and standards, is required. Therefore, it is necessary for auditors to evaluate the quality of management decision-making, using the services of specialists in various fields, and to provide their conclusions and corrective suggestions for further management improvement.16

This study, which relied on interview data, established the essential metrics for assessing the effectiveness of executive bodies, which is crucial for enhancing performance and boosting productivity. The primary categories and subcategories that have been identified are as follows:

-

Subcategories of ‘developing appropriate laws and regulations’: Establishing standards, laws, and requirements; implementing control and oversight over policies and rules.

-

Subcategories of ‘empowering and employing skilled and efficient human resources’: Utilizing specialized personnel, increasing specialized teams through collaboration and establishing relationships, enhancing knowledge and skills, providing performance audit training, and having capable human resources.

-

Subcategories of ‘managing organizational goals’: Quality management for achieving goals, setting and comparing predetermined goals.

-

Subcategories of ‘organizational structuring’: Increasing motivation for research and investigation using precise information systems.

-

Subcategories of ‘implementing control over internal policies’: Establishing and strengthening budget control systems and transparency in financial reporting.

-

Subcategories of ‘internal economic factors’: Proper application and use of operational budgeting, determining economically efficient scales, the role and position of resource measurement, and valuation.

-

Subcategories of ‘creating the basis for performance auditing implementation’: Creating an environment for implementing performance audits, supporting and accepting the need to conduct performance audits, increasing enforceability, and strengthening performance auditing.

-

Subcategories of ‘organizational productivity’: Establishing cost accounting for goods and services and determining and improving critical organizational performance indicators.

Reviewing the research results and comparing the findings and opinions from past research can reveal similarities and differences.

Conclusion

The confirmed indicators in the model are presented as necessary elements for providing an optimal performance auditing framework. The sorting of factors and indicators was approved by experts, considering the apparent requirements and obstacles to conducting performance audits in the health sector, and aligns closely with logic and reality. Indicators such as empowering and employing specialized and efficient personnel, drafting appropriate laws and regulations, managing intra-organizational objectives, organizing the organization, controlling internal policies and internal economic factors, preparing the groundwork for implementing performance audits, and organizational productivity play a crucial role in better execution of performance audits. This aligns mainly with the findings of other research studies. It is important to note that the successful implementation of any organizational control requires the general acceptance of individuals and related organizations, which is also relevant for the optimal execution of performance audits. This research is of high importance due to its innovation and problem-solving in oversight and assessment, and if implemented, it can effectively fulfill its control and operational role.

Acknowledgments

We would like to express our sincere gratitude to the staff of financial affairs of the Tabriz University of Medical Sciences who graciously volunteered to contribute to this study.

Competing Interests

The authors declare no conflict of interest.

Ethical Approval

Not applicable.

References

- Kordestani G, Nasiri M. Efficiency of financial reporting and improving the level of accountability in the public sector. Journal of Accounting 2009;25(208-209):58-65. [Persian].

- Hüpkes E, Quintyn M, Taylor MW. The accountability of financial sector supervisors: principles and practice. Eur Bus Law Rev 2005; 16(6):1575-1620. doi: 10.54648/eulr2005073 [Crossref] [ Google Scholar]

- Babajani J. Advanced Public Sector Accounting with a Multilevel Financial Reporting Approach. Tehran: Allameh Tabataba’i University; 2015. [Persian].

- Homaie S, Babajani J. The Relationship Between Performance Audits and the Improvement of Operational Results and the Assessment of Operational Accountability [thesis]. Tehran: Allameh Tabataba’i University: 2017. [Persian].

- Khojasteh A, Rahnamay Roodposhti F, Nikoomaram H, Zamani Moghaddam A, Taleb Niya G. Present a pattern of financial planning based on management performance auditing. International Journal of Finance & Managerial Accounting 2025; 10(39):139-62. doi: 10.30495/ijfma.2023.72279.1988.[Persian] [Crossref] [ Google Scholar]

- Babajani J, Doust Jabbarian J. A performance auditing implementation model for institutions of the public sectors in Iran. Journal of Management Accounting and Auditing Knowledge 2017;6(21):143-56. [Persian].

- Talei H, Gord A, Kharashadizadeh M. Provide a performance audit model for executive managers of public hospitals. Governmental Accounting 2022; 9(1):255-86. doi: 10.30473/gaa.2022.64538.1588.[Persian] [Crossref] [ Google Scholar]

- Imani Barandagh M. The challenges beyond the obligation of performance audit in the government agencies of Iran. Journal of Health Accounting 2014; 3(4):1-19. doi: 10.30476/jha.2014.16997.[Persian] [Crossref] [ Google Scholar]

- World Bank. World Bank Country and Lending Groups. Washington, DC: The World Bank Group; 2017.

- Fatahzade A. Tehran Health System Reforms. Avicenna Bozor Cultural Institute; 2005. [Persian].

- Jani M, Pifeh A, Faghani M, Dehghan M. Financial supervisors of controllers in the Iranian organizations and the proper implementation of the public sector accounting system: a review of related challenges. Public Sector Accounting and Budgeting 2021;2(4):1-23. [Persian].

- Glaser B. The Discovery of Grounded Theory: Strategies for Qualitative Research. Aldine; 1967. p. 2-6.

- Strauss A. Basics of Qualitative Research: Techniques and Procedures for Developing Grounded Theory. 2nd ed. Translated by Ebrahim Afshar. Tehran: Nashre-Ney Publishing; 2013. [Persian].

- Rao S, Perry C. Convergent interviewing to build a theory in under‐researched areas: principles and an example investigation of Internet usage in inter‐firm relationships. Qual Mark Res 2003; 6(4):236-47. doi: 10.1108/13522750310495328 [Crossref] [ Google Scholar]

- Strauss A, Corbin J. Basics of Qualitative Research: Techniques and Procedures for Developing Grounded Theory. SAGE Publications, Inc; 2008.

- Baradaran Hassanzadeh R, Mahboobi Bonab M, Rahimi G. Investigating execution obstacles of management performance auditing (case study: executive organizations of East Azarbaijan province). The Journal of Productivity Management 2012;6(3) 22):167-94. [Persian].